Business

THC vs. CBD: Legalization is Accelerating, But Where Should You Invest?

In the U.S., legal THC-product sales dominate CBD sales by a 5-to-1 ratio, but outside of North America the THC vs. CBD calculus is very different.

THE FIRST STRATEGIC decision companies typically make as they enter the legal cannabis market is to focus on one or the other of the major cannabinoids, either tetrahydrocannabinol (THC) or cannabidiol (CBD). Having that kind of exclusive focus made sense back in the 2010s. Both compounds come from the same plant, but different regulatory regimes meant different supply chains all the way from seed to sale. Startups with limited resources were smart to focus on one or the other.

In the U.S., where legal THC-product sales dominate CBD sales by a 5-to-1 ratio, many THC investments have already paid dividends. Meanwhile, CBD companies have struggled. But outside of North America, the THC vs. CBD calculus is very different and an “all of the above” strategy toward cannabinoids may make more sense.

In Europe, the potential for legal cannabis has been tantalizing—and frustrating. North American companies have had limited success since Germany legalized medical sales in March 2017 to kick off a supposed EU cannabis boom that has so far been more of a bust. Canada’s licensed producers (LPs) poured hundreds of millions of dollars into European medical-only THC markets, both directly into European assets and into countries in Africa and Latin America that had legalized cultivation hoping to supply Europe.

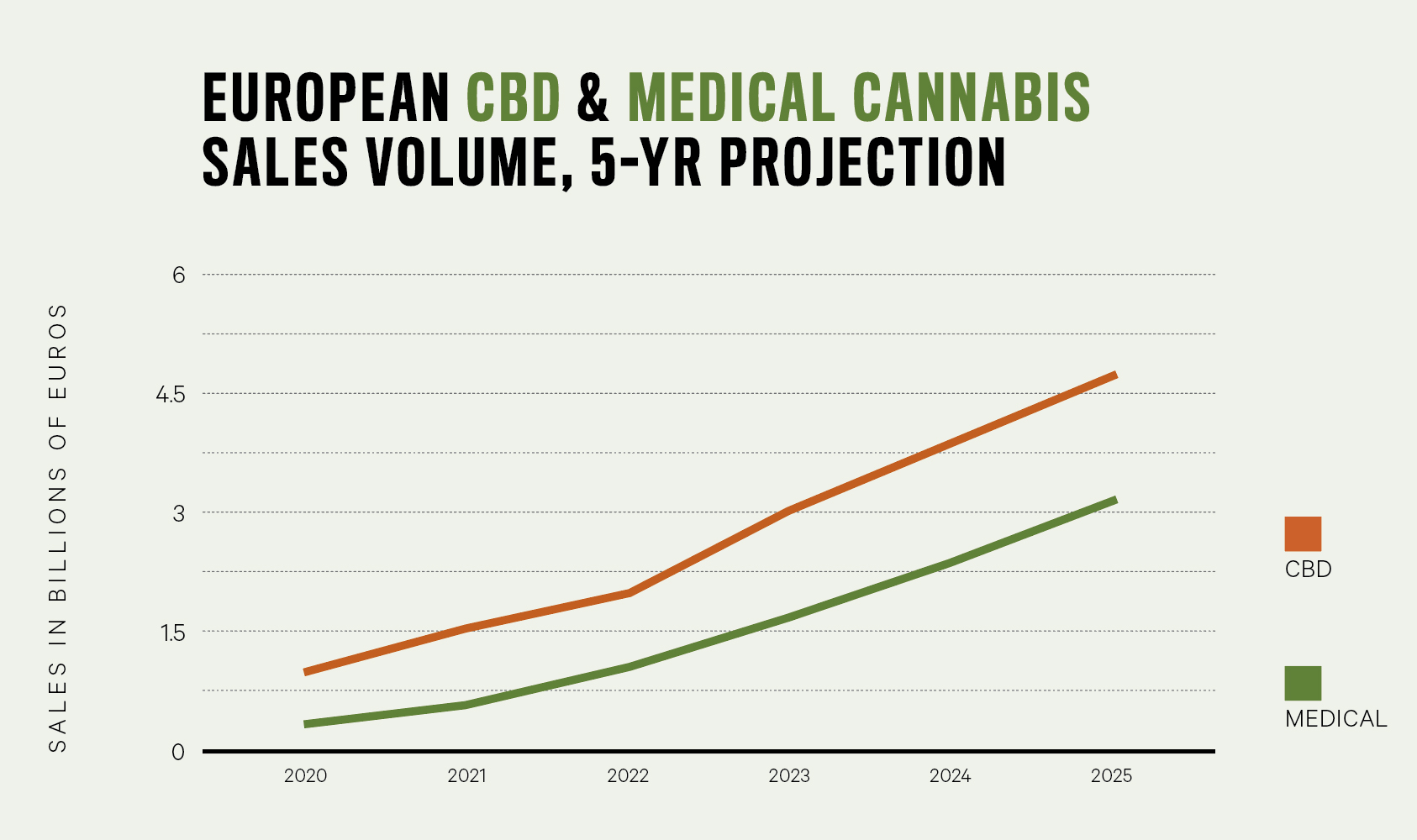

But European medical cannabis has struggled, especially outside of Germany. Last year, German medical cannabis sales reached €342 million (US$360 million), or around 64 percent of the entire European market, according to the Brightfield Group. Eleven other counties combined to make up the remaining 36 percent of Europe’s €540 million medical cannabis market in 2021. European CBD sales of €1.5 billion last year were almost three times those of medical cannabis.

Slow and Slower

The development of both markets slowed in 2020 when COVID-19 came to dominate the health agenda of countries worldwide. But while CBD’s legalization is now accelerating, there is little hope that the pace of medical legalization will quicken. To wit, here’s how that effort is faring in some typical slow-moving countries:

- France’s oft-delayed medical cannabis trial is limited to 3,000 patients through 2023, at which time the government will assess the results.

- Denmark’s program will remain on “pilot” status until at least 2025.

- Ireland will give its trial another five years before assessing results.

Faced with these headwinds, Canadian LPs have dramatically cut back on European medical-cannabis investments. Aurora cancelled its planned Nordic 2 grow operation in Denmark, the second phase of a planned 1 million-square-foot facility announced in 2018. Canopy Growth announced last December that it would divest its C3 German medical distribution operation for €82 million (plus a potential €45 million earn-out). Canopy Growth had paid €235 million in cash for C3 in May 2019, an optimistic 8.5 times C3’s 2018 revenue of €28 million.

The European medical market will likely still prove a good fit for companies already in the prescription pharmaceutical business such as Madrid, Spain-based Alcaliber. Purpose-built medical cannabis providers like Veendam, Netherlands-based Bedrocan will also have a leg up in the market.

The Elusive Prize

But what about companies whose real interest is to be in a good position when adult-use legalization unlocks an expected consumer packaged goods (CPG) boom for cannabinoid products in Europe? They are eyeing the prospects for an EU that has more people than the U.S. (447 million versus 328 million) and an economy three-quarters the size (U.S. GDP in 2019 was €20.3 trillion vs. the EU’s €14.9 trillion, per the World Bank).

Are those companies better off behind the pharmacy counter dispensing medical cannabis or out in general retail channels hawking CBD products?

Admittedly, European CBD has had its own growth challenges. EU regulators designated CBD a “Novel Food” in January 2019, a move that burdens CBD makers with a lengthy safety review process before ingestibles can be sold legally.

Still, operating behind the forbearance granted by a European Court of Justice ruling that CBD should not be considered a narcotic, CBD product makers and retailers have built a “gray market” that Brightfield forecasts will remain substantially larger than medical cannabis. This should be the case as Novel Food applications start to get approved and CBD sales, both online and retail, become fully legal.

A few U.S. companies have noticed the CBD opportunity in Europe. Cookies, one of the most successful U.S. cannabis brands, struck a deal last year with Israeli cannabis company Intercure to open Cookies-branded stores in the UK and Austria in 2022. What will they stock? Whatever’s legal—which for now, means CBD products.

Market data & findings by Global Go Analytics

A Whole New Ballgame

What’s clear is that European cannabinoid markets will be very different from North America’s. Strategic planning for a cannabinoid business in Europe really comes down to two issues:

- Deciding on which sub-sectors of the industry to focus on—cultivation, processing, wholesale distribution, CPG or retail

- Assessing the likely relative consumer demand for cannabinoid product types: medical cannabis, adult-use cannabis and/or CBD

The LPs’ woes in Europe sprang from miscalculations on both fronts: overestimating the speed at which medical cannabis would be embraced by regulators, doctors and patients, and conceiving of themselves mainly as cultivators. Canopy Growth acknowledged as much in announcing it would sell C3 as part of “continuing its evolution into a CPG-modeled organization.” In fact, all the publicly traded Canadian LPs have been re-positioning themselves as branded-product companies since their home market saw the debut of edibles, vapes and topicals in October 2019.

U.S. multi-state operators (MSOs) like Cookies started aggressively building their brand presence in state-licensed medical dispensaries many years ago. They were free to do so, ironically, because they have been less encumbered than the LPs by federal regulations. In European pharmacies, under the stern watch of federal medical regulators, that brand-building success will be hard to emulate.

CBD products, in contrast, are already being sold over the counter in the same kinds of stores in which European consumers get their other CPG products. Not all North American brands have fared as well in Europe as, say, McDonald’s or Apple. But as the Novel Foods application process starts to show post-COVID progress, it is certainly a wide-open field, with hundreds of small brands battling for market share without the benefit of cash-generating North American brands to fuel their efforts.

A Better Roadmap

Germany’s new ruling coalition is on the record intending to legalize adult use and Switzerland and the Netherlands are planning to launch adult-use trial programs in the next 12 months. But getting started in Europe with CBD may prove to be more than just an exercise in getting ready for adult-use cannabis sales.

In fact, CBD products have introduced cannabinoid usage to a European populace that has never embraced THC to the extent people in other parts of the world have. Reported annual consumption of cannabis in most European countries is well under half that of Canada or Israel, countries where more than a quarter of adults say they have consumed in the last 12 months. Per capita cannabis usage in Germany, Europe’s largest country, is less than one-third that of the U.S.

So, the first thing North American cannabis companies looking to enter Europe need to do is downsize their expectations. Simply mapping over per-capita spending benchmarks from existing adult-use markets in the U.S. and Canada will surely overestimate Europe’s potential. This, even if Germany and the handful of other countries now discussing adult-use legalization get it done any time soon.

Second, CBD should probably be given a more central role in European strategies than in a North American market where the daily THC consumer is the core target audience. With CBD’s sizeable lead in existing sales and much quicker route to full legalization, Europe may well become the venue in which humanity’s millennia-long attraction to cannabis is shown to have as much to do with CBD’s relaxing, anxiety-reducing effects as with the euphoric effects of THC.

Cannaconvo with Peter Su of Green Check Verified

Cannabis Last Week with Jon Purow interviews Peter Su of Green Check Verified. Peter Su is a Senior Vice President with Green Check Verified, the top cannabis banking compliance software/consultancy in the space. A 20+ year veteran of the banking industry, Peter serves on the Banking & Financial Services committee of the National Cannabis Industry Association. He chairs the Banking and Financial Services Committee for the NYCCIA & HVCIA. He is an official member of the Rolling Stone Cannabis Culture Council. And, he is on the board of the Asian Cannabis Roundtable, serving as treasurer.

Ohio’s Move to Adult-Use Sales Could Be Record-Setting

Cannabis Investor Focus Shifts to Retail